Money management doesn’t have to feel overwhelming or complicated. Many people struggle with budgeting because they try to track every single penny, creating systems so rigid they abandon them after a few weeks. What if you had a method that was simple enough to understand in minutes but powerful enough to transform your financial life? The 50/30/20 budget rule offers precisely that. This approach divides your money into three straightforward categories: essentials you must pay, things you enjoy, and funds you set aside for your future.

Whether you earn a modest salary or a significant income, the 50/30/20 budget rule can be your starting point for financial stability. Instead of feeling restricted by your budget, you get permission to spend on things that bring you joy while still building wealth for tomorrow.

In this article, we will discuss what the 50/30/20 budget rule is, how to create and implement it step-by-step, provide real-world examples, identify common mistakes people make, and outline situations where you might need to adjust the formula to fit your specific circumstances.

What Is the 50/30/20 Budget Rule?

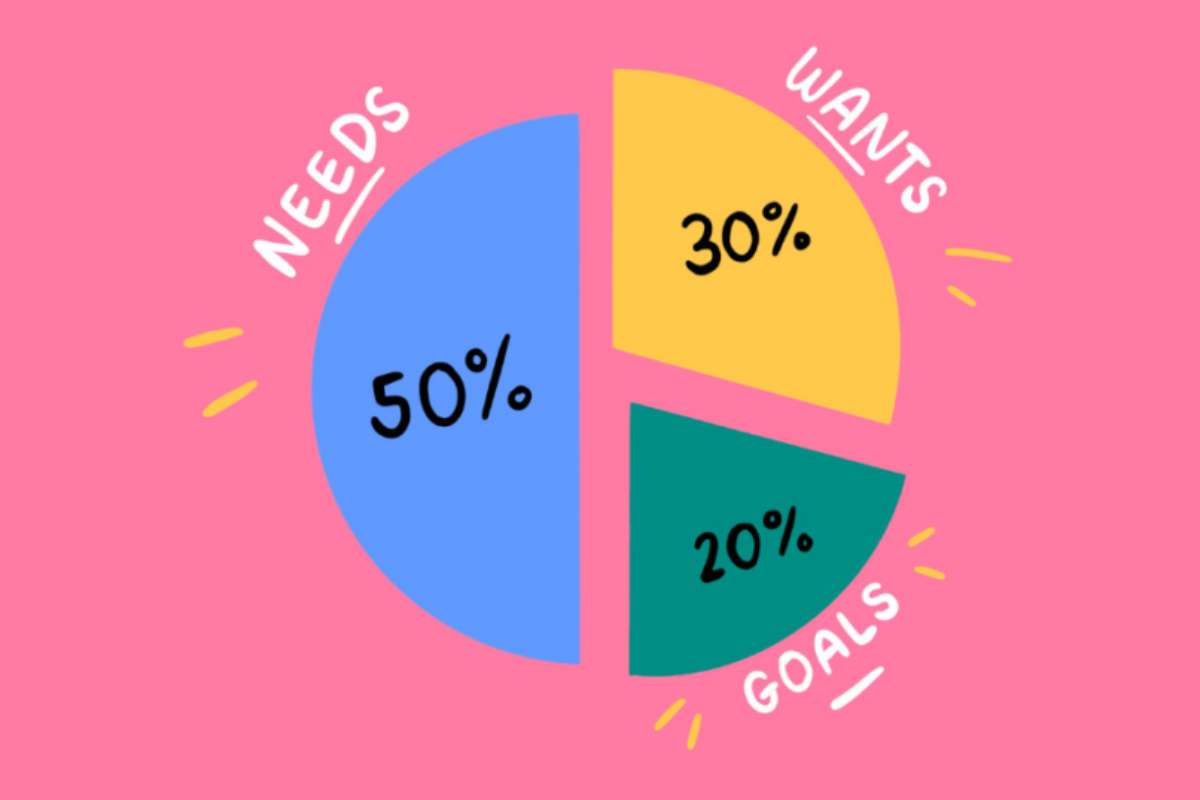

The budget rule is a simple framework for organizing your after-tax Income into three main spending categories. Created by U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2006 book, “All Your Worth: The Ultimate Lifetime Money Plan,” this method has helped millions of people manage their finances with simplicity and clarity. It divides your monthly take-home pay as follows: 50% goes to your needs, 30% goes to your wants, and 20% goes to savings and debt repayment.

This approach works because it balances three essential elements of healthy finances. Your needs are the expenses you cannot avoid—things required for basic survival and functioning. Your wants are the pleasures and comforts you choose to purchase. And your savings represent your commitment to your future. The 50/30/20 budget rule deliberately includes 30% for wants because financial experts understand that completely denying yourself joy leads to burnout and abandoning your budget altogether. By building in flexibility while maintaining structure, the 50/30/20 budget rule becomes a system you can actually follow.

➣ How to Create a 50/30/20 Budget Step-by-Step?

Creating your budget rule requires only a few straightforward steps. Let’s walk through each one to get you started on your financial planning journey.

Step 1: Calculate Your After-Tax Income

Begin by determining your monthly take-home pay. This is the amount that actually lands in your bank account after taxes and mandatory deductions have been applied. If you receive a regular salary, check your pay stub to find your net Income. If you earn money irregularly through freelancing or commissions, calculate an average of your Income over the past three to six months. This figure becomes the foundation for applying the 50/30/20 budget rule.

Step 2: Identify Your Needs (50%)

Next, list all your essential expenses. These are costs you absolutely must pay to maintain your home, health, and ability to work. Your needs typically include rent or mortgage payments, utility bills, groceries, insurance premiums, transportation costs, and minimum debt payments. Be honest about what truly qualifies as a need. A need is something that has serious consequences if you don’t pay it—your landlord could evict you for unpaid rent, or your electricity gets shut off without payment. Using this money management rule, you should spend no more than 50% of your Income on these essentials.

Step 3: Define Your Wants (30%)

Now identify your discretionary expenses—the things you spend money on by choice. Your wants include streaming subscriptions, dining at restaurants, entertainment purchases, hobbies, vacations, and shopping for non-essential items. These are expenses that improve your quality of life but aren’t necessary for survival. The 50/30/20 budget rule assigns 30% of your Income to this category. This allocation gives you genuine freedom to enjoy your life without guilt while maintaining financial discipline.

Step 4: Allocate Your Savings (20%)

The remaining 20% of your Income should go toward your future. This category includes contributions to your emergency fund, retirement accounts, investments, and payments beyond the minimum on debts. The 50/30/20 rule emphasizes savings as a non-negotiable part of your monthly plan. Even if you have other financial obligations, protecting this 20% creates a buffer against unexpected expenses and builds wealth over time.

Step 5: Set Up Automatic Transfers

Once you know the dollar amounts for each category, set up automatic transfers from your checking account to ensure timely payments. Schedule a transfer to your savings account on payday so the money moves before you’re tempted to spend it. This approach aligns with the 50/30/20 budget rule’s philosophy of making budgeting effortless rather than requiring constant willpower.

➣ Example of the 50/30/20 Budget Rule:

Let’s look at a practical example to see how the 50/30/20 rule works in real life.

Monthly Income: $5,000 (after taxes)

Here’s how the budget breaks down:

50% for Needs: $2,500

- Rent: $1,200

- Utilities and internet: $180

- Groceries and food at home: $450

- Transportation (car payment and fuel): $400

- Health insurance: $270

30% for Wants: $1,500

- Dining out and coffee: $350

- Streaming subscriptions and entertainment: $150

- Shopping and clothing: $300

- Hobby supplies and gym membership: $250

- Weekend entertainment and outings: $450

20% for Savings: $1,000

- Emergency fund: $400

- 401(k) retirement contribution: $450

- Investment account: $150

By following the 50/30/20 rule, you have a clear plan for every dollar earned. Essential expenses stay covered, discretionary spending gets allocated, and wealth builds steadily. After six months of adhering to this budget, the emergency fund has grown to $2,400. After a year, retirement savings and investments grow significantly.

This example demonstrates how the 50/30/20 rule creates balance. You get to enjoy your life through the wants category without guilt, while your future remains protected through consistent savings.

➣ Common Mistakes to Avoid

When implementing the 50/30/20 budget rule, people often make errors that derail their progress. Understanding these mistakes helps you avoid them.

Mistake 1: Misclassifying Expenses

.jpg)

The biggest issue people face with the 50/30/20 budget rule is determining whether something falls into the ‘needs’ or ‘wants’ category. A gym membership could be classified as a want if it’s for fitness enjoyment, but it might be considered a need if it’s part of your health recovery plan. Premium cable channels are wants, but basic utilities are needs. When you’re unclear, ask yourself: could I survive without this? If the answer is yes, it goes in wants.

Mistake 2: Using Gross Income Instead of Net Income

Some people attempt to apply the 50/30/20 rule using their gross Income before taxes. This creates an impossible budget because you don’t actually have access to that full amount. This budget rule relies on calculating percentages from your take-home pay, which is the actual amount you receive after taxes are deducted.

Mistake 3: Making No Room for Adjustments

While the budget rule provides precise percentages, it’s not written in stone. Many people fail because they expect these exact percentages to work forever. Life changes—you get promoted, move to a more expensive city, or experience unexpected costs. The 50/30/20 rule is meant to be a flexible framework, not a rigid mandate.

Mistake 4: Borrowing From Savings to Fund Wants

The most damaging mistake is treating your 20% savings allocation as if it were flexible. If you consistently dip into savings to cover extra wants, you’ll never build wealth. The 50/30/20 budget rule only works when you protect that savings portion fiercely and adjust your wants spending if necessary.

Mistake 5: Not Tracking Your Progress

Many people create a budget using the 50/30/20 budget rule, but never check whether they’re actually following it. After a few months, they tend to revert to their old spending habits. Tracking keeps you accountable and helps you spot problems early.

➣ When the 50/30/20 Rule Might Not Work?

While the 50/30/20 budget rule works well for many people, certain situations require adjustments or an alternative approach entirely.

1. High Cost-of-Living Areas

In expensive cities, housing alone might consume 40% or more of your Income, making it impossible to stay within the 50/30/20 budget rule formula. If this applies to you, you may want to adjust to a 60/25/15 split, providing more breathing room for necessities.

2. Low-Income Earners

For individuals with modest incomes, the budget rule can seem unrealistic. When rent, utilities, and groceries take up 60% or 70% of your earnings, saving 20% becomes impossible. In these situations, consider a 70/20/10 approach or focus on saving whatever percentage you can afford, even if it’s just 5% per month.

3. High Earners

Someone earning $30,000 per month might find their essential expenses only take 20% of their Income. Following the 50/30/20 rule strictly would mean spending 30% on wants, leaving 50% unaccounted for. For high earners, the percentages should shift toward increased savings and investments.

4. Variable Income

Freelancers, commission-based workers, and gig economy participants face unstable monthly Income. The 50/30/20 budget rule assumes consistent earnings. These professionals might use their average annual Income to create a more flexible monthly budget.

5. Significant Debt Repayment

If you’re aggressively paying down credit card or student loan debt, putting only 20% toward debt payoff might be insufficient. You could dedicate 30% to debt repayment and wants combined, prioritizing debt elimination.

6. Major Life Goals

Someone saving for a down payment on a house or planning a career change might need to increase their savings percentage beyond 20%. The 50/30/20 budget rule provides a starting framework, but your actual percentages should reflect your genuine priorities.

Also Read: The Golden Rule in a CIO’s Life: Balancing Innovation with Human Impact

Conclusion

The 50/30/20 budget rule remains one of the most practical approaches to money management in 2026. Its simplicity makes it accessible to anyone. By dividing your Income into needs, wants, and savings, you create a sustainable system that prevents financial stress. The budget rule doesn’t demand sacrifice or ignore your future. Starting with this framework helps you avoid overspending while ensuring your needs stay covered and savings grow steadily.