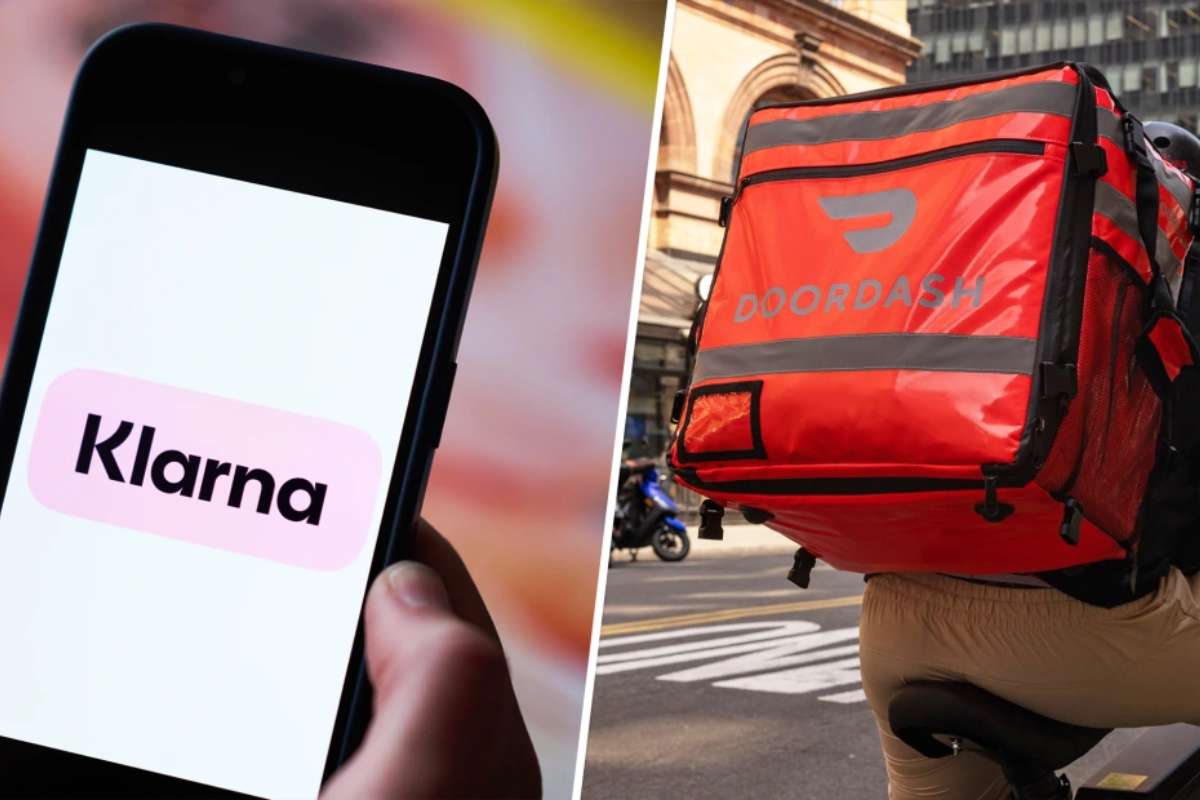

A New Payment Option for Customers

DoorDash has partnered with financial technology company Klarna to introduce a “buy now, pay later” (BNPL) option for customers. The new feature, announced on Thursday, allows users to split the cost of their orders into four interest-free payments or defer the payment to a later date. This option is available for purchases made through DoorDash’s website and mobile app.

DoorDash, primarily known for food delivery, has expanded its services to include retail items such as electronics, makeup, and medicine. According to Anand Subbarayan, head of money products at DoorDash, offering flexible payment options is an essential step as the company broadens its product range. Klarna, which already works with other food-delivery services like Instacart and Uber Eats, sees this partnership as part of its growing influence in the BNPL market.

While the feature is designed to make payments more manageable, consumer advocates have raised concerns about the potential risks associated with using BNPL for essential purchases like food. Research indicates that BNPL loans are often used by individuals who are already in debt, raising questions about their long-term financial impact.

Concerns Over Financial Risks

DoorDash and Klarna Consumer Reports’ advocacy program director, Chuck Bell, acknowledged that BNPL loans could be useful if managed responsibly but warned against excessive reliance on them. He advised users to track their payment schedules and ensure they have sufficient funds to cover their loans.

“If you don’t pay the bill on time and start getting multiple late fees, it could end up being a very expensive chile relleno or pad Thai,” Bell cautioned.

A key concern is that people might use BNPL loans for recurring expenses, such as food, without considering how it could affect their future financial stability. Bell questioned whether individuals would continuously defer payments for essentials, creating a cycle of financial strain.

Following the announcement by DoorDash and Klarna, some social media users expressed concerns that customers might finance even small purchases, such as $10 or $20 meals. In response, Klarna clarified that the pay-in-four option would only be available for purchases over $35. The company also argued that paying for groceries in interest-free installments was a better alternative to using credit cards, which often charge high interest and fees. Klarna emphasized that its business model relies on customers making payments on time, unlike credit card companies that profit from revolving debt.

Regulatory Scrutiny on BNPL Loans

DoorDash and Klarna has been expanding rapidly BNPL market, attracting regulatory attention. A report from the Consumer Financial Protection Bureau (CFPB) in January 2025 revealed that 21.2 percent of consumers used BNPL loans for at least one purchase in 2022, an increase from 17.6 percent in 2021. However, the report also highlighted concerns about debt accumulation, as many BNPL users carried higher balances on personal loans, student loans, and credit cards.

The CFPB found that about 20 percent of BNPL borrowers in 2022 were heavy users, taking out at least one loan per month, while 63 percent had multiple active loans during the year. Despite these concerns, the bureau noted that BNPL loan defaults were lower than credit card defaults, likely due to the automatic repayment system used by BNPL providers. Between 2019 and 2022, 2 percent of BNPL loans defaulted, compared to 10 percent of credit card balances.

With Klarna preparing for an initial public offering and “buy now, pay later” (BNPL) services growing in popularity, regulators continue to assess the risks and benefits of this payment model. The CFPB has ruled that BNPL lenders DoorDash and Klarna must provide consumer protections similar to those required for credit cards, including allowing customers to dispute charges. As BNPL loans become a more common payment method, financial experts urge consumers to use them wisely and avoid overextending their debt.