Money decisions can get confusing fast: how much to save, what to spend, or when to invest. But here’s the good news: you don’t always need complicated strategies to manage your finances. Sometimes, a few simple financial rules of thumb can make all the difference.

These are easy-to-remember guidelines that keep your money habits on track. Like saving 20% of your income, keeping your rent or mortgage below 30%, or building an emergency fund for 3 to 6 months of expenses. Small rules like these can quietly shape a strong financial foundation over time.

It matters more than you might think. A 2024 CNBC report found that 65% of working adults live paycheck to paycheck, and only one in three has a proper financial plan. But studies show that people who follow clear money rules are far more confident and secure about their future.

Think of financial rules of thumb as everyday money anchors; they help you make better decisions without second-guessing everything. Of course, they’re not perfect. Everyone’s situation is different, and sometimes, these rules need to be adjusted.

In this blog, we’ll explore what these rules actually mean, why they’re useful, and how to apply them to your own life, so you can make smarter, stress-free money choices.

What Are the Financial Rules of Thumb?

At its core, financial rules are simple money guidelines that help you make quick and sensible financial decisions without overthinking every detail. They’re not strict laws or one-size-fits-all formulas; they’re practical shortcuts based on years of financial experience and patterns that tend to work for most people.

Think of them like your “money cheat codes.” They save you from getting lost in complicated numbers and give you a clear direction when you’re unsure what to do. Whether it’s deciding how much to save, spend, or invest, these rules make financial planning easier to stick with.

Here are a few examples you might already know without realizing it:

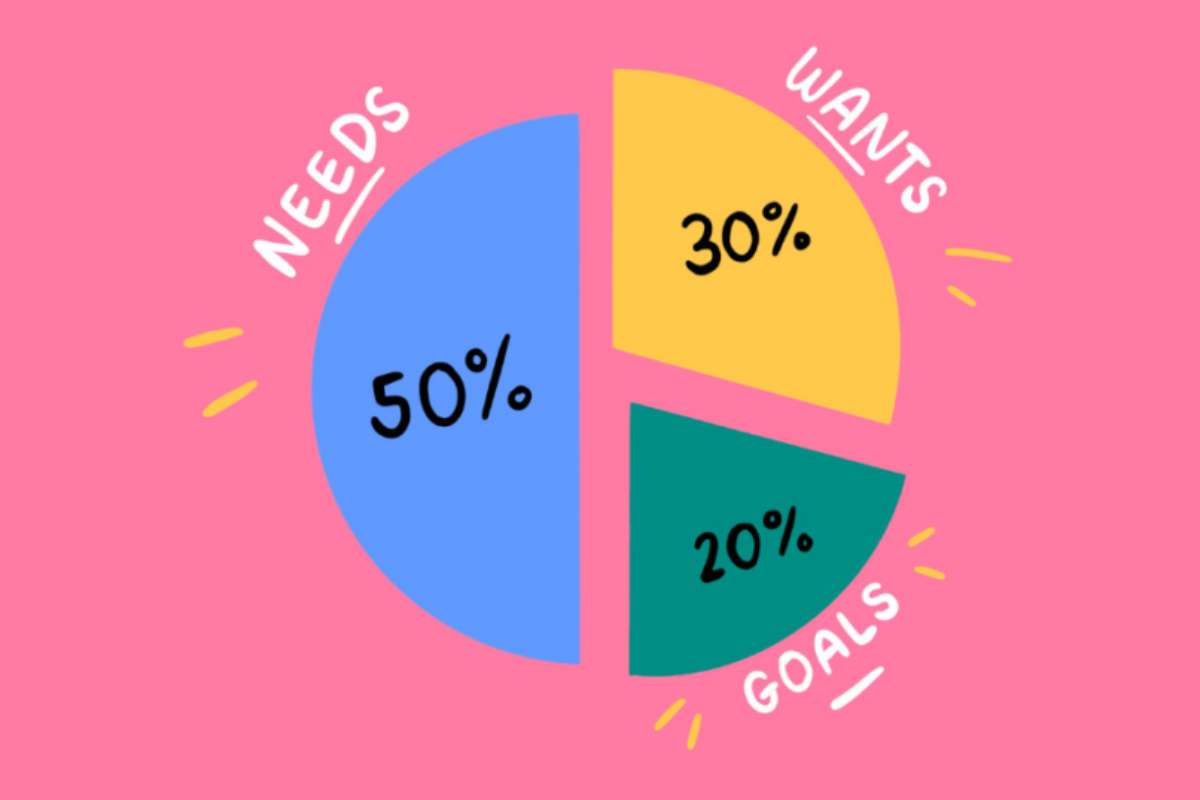

| The 50/30/20 rule | Spend 50% of your income on needs, 30% on wants, and save or invest the remaining 20%. |

| The 3–6 month rule | Keep an emergency fund that can cover your living expenses for at least three to six months. |

| The 30% housing rule | Try not to spend more than 30% of your income on rent or mortgage payments. |

| The pay-yourself-first rule | Save a portion of your income before paying bills or expenses. |

These financial rules of thumb are popular because they’re easy to apply and easy to remember. You don’t need to be a financial expert to use them, just consistency and a little discipline.

The best part? They can be customized to your situation. For instance, if you live in a high-cost city, your housing ratio might go beyond 30%, and that’s okay. The point isn’t to follow every number exactly; it’s to create healthy financial habits that fit your lifestyle and goals.

In short, financial rules of Thumb are your everyday tools for smarter money management. They simplify complex choices, help you stay on track, and make your financial life a little less stressful.

Why Financial Rules of Thumb Matter?

Money can be emotional. Between bills, savings goals, and unexpected expenses, it’s easy to feel uncertain about whether you’re making the right decisions. That’s where financial rules come in; they simplify the process and give you a steady foundation to build from.

These rules matter because they help you take control of your money, even if you’re not a finance expert. When you have clear guidelines like saving 20% or keeping debt below 40% of your income, you remove guesswork and reduce financial stress. It’s about making money management automatic, not overwhelming.

A 2023 study by CISI found that clients of a professional financial planner had a better quality of life, financial confidence, and happiness (75%) than those who were not advised (71%), with 83% of advised respondents reporting a sense of financial security compared to 74% of unadvised.

In simple terms, financial rules of thumb help you:

- Stay consistent with saving and spending.

- Avoid major money mistakes like overspending or taking on too much debt.

- Build financial confidence and peace of mind.

- Create habits that support long-term goals without constant effort.

Another reason these rules matter is that they work in both good and bad times. When income rises, they keep your spending in check. When times get tough, they guide you toward smart cutbacks and financial stability.

Of course, they’re not perfect; they don’t replace personalized financial advice or account for every unique situation. But they do provide a reliable starting point. Even experienced financial planners often use these same principles when helping clients build a foundation for wealth.

At the end of the day, financial rules make your finances easier to manage and less stressful to think about. They help you focus on what really matters, using your money to build security, freedom, and peace of mind.

Top 10 Financial Rules of Thumb: Budgeting and Spending Rules

Money management doesn’t have to be complicated. A few well-chosen financial rules can simplify decisions, help you plan better, and reduce the stress of figuring out where your money goes each month. Below are ten essential rules every financially aware person should know, explained in an easy, relatable way.

1. The 50/30/20 Rule

| Core Principle | Divide income into needs, wants, and savings |

| Suggested Percentage or Ratio | 50% Needs, 30% Wants, 20% Savings |

| Purpose/Benefit | Balanced budgeting |

Among the most popular financial rules of thumb, the 50/30/20 rule is the one that offers a simple structure that aligns with how people actually live. It encourages you to meet your essential needs, enjoy your wants, and still save enough for the future. What makes it powerful is its flexibility; you can shift the percentages slightly based on life stages. A college graduate may save less initially, while someone nearing retirement might boost savings to 25–30%. The core idea remains balanced, not restricted.

2. Pay Yourself First

| Core Principle | Save before you spend |

| Suggested Percentage or Ratio | 10–20% of income |

| Purpose/Benefit | Builds savings discipline |

This financial rule of thumb flips your mindset from reactive to proactive. Instead of saving what’s left at the end of the month, it pushes you to treat savings as a non-negotiable expense. The beauty lies in automation; set up an automatic transfer to your savings or investment account the moment your paycheck arrives. Over time, this habit builds wealth quietly, and you barely notice the difference in your spending power. It’s the easiest way to ensure your financial goals never get “postponed.”

3. The 30% Housing Rule

| Core Principle | Limit housing costs |

| Suggested Percentage or Ratio | ≤ 30% of income |

| Purpose/Benefit | Prevents overspending on rent/home |

This rule helps you anchor your lifestyle within realistic boundaries. By capping your housing expenses, you ensure that one part of your budget doesn’t drain your financial flexibility. It’s especially relevant today, as urban rents and EMIs rise. Think of it as a “safety limit” that lets you enjoy your home without sacrificing your plans like travel, savings, or investments.

4. The Emergency Fund Rule

| Core Principle | Keep a safety cushion |

| Suggested Percentage or Ratio | 3–6 months’ expenses |

| Purpose/Benefit | Protection from financial shocks |

Life can be unpredictable, with layoffs, medical issues, surprise bills, and this is where key financial rules of thumb like this one make all the difference. The goal isn’t just about having cash; it’s about peace of mind. Having three to six months’ worth of expenses tucked away ensures that you never have to rely on high-interest credit or loans in times of crisis. Building it gradually, even ₹2,000–₹5,000 a month, can make a world of difference over time.

5. The 20/4/10 Rule for Car Purchases

| Core Principle | Manage car affordability |

| Suggested Percentage or Ratio | 20% down, 4-year loan, 10% income |

| Purpose/Benefit | Avoids car-related debt traps |

This one’s about preventing “car fever,” that moment when shiny exteriors and zero-down offers make you spend beyond reason. The rule promotes responsible ownership by keeping your vehicle expenses tied to your income and debt capacity. It helps you enjoy your car without turning it into a financial burden that eats away at your savings.

6. The 1% Home Maintenance Rule

| Core Principle | Save for upkeep |

| Suggested Percentage or Ratio | 1% of home value annually |

| Purpose/Benefit | Prevents costly repairs later |

A less-talked-about but practical financial rule of thumb, this one reminds homeowners that buying a house is only the beginning. Roof repairs, painting, plumbing, they all add up. By setting aside 1% of your home’s value each year, you stay prepared for these inevitable costs. This rule turns homeownership from a financial strain into a sustainable, long-term investment.

7. The 4% Retirement Withdrawal Rule

| Core Principle | Sustainable withdrawals post-retirement |

| Suggested Percentage or Ratio | 4% per year |

| Purpose/Benefit | Ensures lifetime income stability |

This rule isn’t about saving; it’s about smart spending in retirement. The 4% guideline helps retirees withdraw money steadily without draining their funds too fast. For instance, if you have ₹1 crore saved, you could safely withdraw ₹4 lakh a year. It provides structure for those who want to enjoy retirement comfortably while ensuring their nest egg lasts.

8. The Debt-to-Income Rule

| Core Principle | Limit total debt |

| Suggested Percentage or Ratio | ≤ 36% of income |

| Purpose/Benefit | Keeps debt manageable |

Another vital financial rule of thumb, this one serves as a red flag for overborrowing. By keeping total debt payments under 36% of your income, you preserve breathing space for savings and emergencies. It’s also a number lenders use to assess your creditworthiness. If you cross this threshold, it’s a sign to slow down borrowing or focus on repayment before adding more liabilities.

9. The Rule of 72

| Core Principle | Estimate money-doubling time |

| Suggested Percentage or Ratio | 72 ÷ annual return rate |

| Purpose/Benefit | Quick compounding calculation |

A favorite among investors, this rule simplifies the magic of compound interest. It helps you quickly estimate how long it will take for your money to double, depending on your investment’s annual return. This quick mental math isn’t just convenient; it gives you perspective on the power of patience. You begin to see why steady, long-term investing always beats chasing short-term trends.

10. The 10% Fun Spending Rule

| Core Principle | Allocate guilt-free spending |

| Suggested Percentage or Ratio | 10% of income |

| Purpose/Benefit | Balances enjoyment and control |

Money isn’t just about bills and savings; it’s also about joy. This rule keeps your budget human by setting aside 10% for the things that make life enjoyable: travel, hobbies, or self-care. The key is intentionality; knowing you’ve already planned for fun allows you to enjoy guilt-free spending without compromising your goals.

One of the most overlooked financial rules is resisting the urge to upgrade your lifestyle every time your income increases. Instead, divert that extra money toward investments, emergency savings, or debt repayment. It’s how financially secure people are

When Financial Rules of Thumb Don’t Apply

While financial rules are great for giving direction, they’re not one-size-fits-all. Real life rarely fits neatly into percentages and formulas. Income levels, family responsibilities, location, and personal goals all shape what’s financially “right” for you. These rules are guides, not gospel, and there are times when it’s smarter to bend or even break them.

Let’s look at a few common situations where financial rules of thumb might not fully apply and how to adapt them wisely.

1. The 50/30/20 Rule Doesn’t Work for Everyone.e

If you live in a high-cost city like Mumbai or New York, sticking to 50% for needs may feel impossible. Rent alone might take up 40–45% of your income. Instead of feeling defeated, adjust your categories; maybe 60/25/15 fits your reality better. The idea is to keep the structure, not the exact numbers.

2. The 30% Housing Rule Can Be Unrealistic in Urban Areas.

With real estate prices soaring, many people spend more than 30% of their income on housing without being financially reckless. In such cases, offset the difference by saving on discretionary spending or building a stronger emergency fund. Remember, context matters more than conformity.

3. The Emergency Fund Rule May Need Adjusting

While three to six months of expenses is a solid benchmark, it’s not universal. Freelancers or self-employed individuals might need closer to 9–12 months of backup savings due to irregular income. On the other hand, someone with a stable government job and benefits may be fine with less. Tailor your buffer to your lifestyle’s unpredictability.

4. The 4% Retirement Rule May Not Fit Every Market.

Market volatility, inflation, and increasing life expectancy can make this rule too simplistic. In low-return years, withdrawing 4% could drain your savings faster than planned. Financial advisors often recommend a flexible withdrawal strategy, lowering it to 3–3.5% during market downturns and increasing it slightly in better years.

5. The 1% Home Maintenance Rule Can Vary by Property Age.

Newer homes might need far less maintenance, while older properties could require double that. Climate also plays a role; homes in humid or coastal areas often need more upkeep. The key is to track your actual expenses over a few years and adjust your maintenance budget accordingly.

6. The 20/4/10 Rule May Not Suit Everyone’s Transportation Needs.

If you live in a city with great public transport, you might not even need a car, saving yourself a major expense. But if you live in an area without reliable commuting options, flexibility matters. You can modify this financial rule of thumb by increasing your car budget slightly while cutting back in other areas.

7. The Debt-to-Income Ratio Can Differ by Stage of Life

Younger professionals often take on more debt, early education loans, first homes, or startup investments, but compensate later as their income grows. Crossing the 36% mark temporarily isn’t dangerous if you have strong earning potential or a clear repayment plan. It’s only risky when your debt grows faster than your income.

8. The Rule of 72 Doesn’t Account for Taxes or Inflation

While it’s a quick way to estimate returns, it assumes constant growth, which isn’t realistic in volatile markets. Use it for ballpark figures, but always factor in taxes, fees, and inflation before setting real expectations.

9. The 10% Fun Spending Rule Might Change with Life Stage.

If you’re aggressively saving for a big goal, l say buying a house or paying off student loans, cutting back to 5% for fun might make sense temporarily. Conversely, if your finances are stable and you value experiences, going up to 15% won’t ruin your budget. Flexibility is the real key.

10. The 50/30/20 and “Pay Yourself First” Rules Need Periodic Review

As your income grows or life circumstances shift, so should your percentages. A financial plan that worked at 25 may not fit at 40. Revisiting your budget annually ensures your money habits evolve with your goals, not against them.

Financial rules of thumb are like road signs; they point you in the right direction, but don’t dictate the route. They’re best used as starting points, not final answers. The smartest approach is to personalize them to your income, lifestyle, and ambitions. The more your financial plan reflects your reality, the more likely it is to succeed.

Conclusion:

At the end of the day, financial rules of thumb are not just catchy formulas; they’re powerful starting points that help simplify the chaos of money management. They give you structure when you’re unsure where to begin, whether it’s budgeting through the 50/30/20 rule, planning for retirement with the 4% withdrawal rule, or building an emergency cushion for tough times.

But remember, these rules aren’t one-size-fits-all. Your financial situation, income level, goals, and lifestyle will always shape how these rules apply. Think of them as flexible frameworks rather than rigid laws. Use them to guide your decisions, not define them.

When used wisely, these financial rules can transform how you save, spend, and invest, helping you move from financial confusion to confidence. The real goal isn’t just following the rules, but understanding why they work and adapting them to build a future that truly fits you.