Family finance management matters now more than ever, especially with daily expenses climbing and families trying to make every rupee count. It’s not about being perfect or cutting joy from life. It’s about knowing where your money goes, making choices that fit your family’s needs, and building a small safety cushion so surprises don’t turn into stress. When you stay aware and plan a little, you protect your home, your peace, and your future.

Family finance management also means talking openly about money, setting goals you understand, and adjusting your plans when life changes. You do not need complicated tricks or expert skills. What helps most is consistency, basic tools, and honest conversations with your family so everyone moves in the same direction. In this article, you’ll learn simple ways to budget, save, talk to your family about money, and stay steady through ups and downs.

Why Family Finance Management Has Never Been More Important ?

The cost of living continues to rise in 2025, and the average family is feeling the financial strain. Inflation has made everything from groceries to healthcare more expensive, leaving less money left over at the end of each month. This is precisely why family finance management has become critical. Without a clear plan, families can easily slip into overspending, accumulating debt, and experiencing constant financial stress. According to recent research, over 60% of families identify groceries as their most significant economic burden, followed by utilities and transportation costs. When you implement solid family finance management practices, you gain visibility into your spending and take back control.

The impact of poor money management extends beyond just bank accounts. Financial stress strains relationships, affects children’s emotional well-being, and can even harm your health. Studies show that economic arguments are a leading cause of marital conflict, yet many couples avoid discussing money altogether. When you embrace family finance management as a household priority, you’re doing more than protecting your wallet. You’re strengthening your marriage, teaching your children valuable lessons about responsibility, and creating an environment where everyone feels secure about the future.

7 Strategies for Managing Family Finance Management:

1. The Foundation: Building a Budget That Works

Creating a budget is the first step in successful family finance management, and it doesn’t have to be complicated. A budget is a spending plan that shows where your money comes from and how it is spent each month. The key is building one that feels realistic for your family, not one that’s so restrictive it causes you to abandon it after a few weeks.

Start by tracking your actual spending for one month. Write down everything you spend money on, whether it’s your salary, bonus, freelance income, or money from other sources. Use a simple spreadsheet, a dedicated app, or even a notebook. The goal is to gain a clear understanding of your current habits before making any changes. Once you see exactly where your money goes, you can identify areas to cut back and places where you’re already spending wisely.

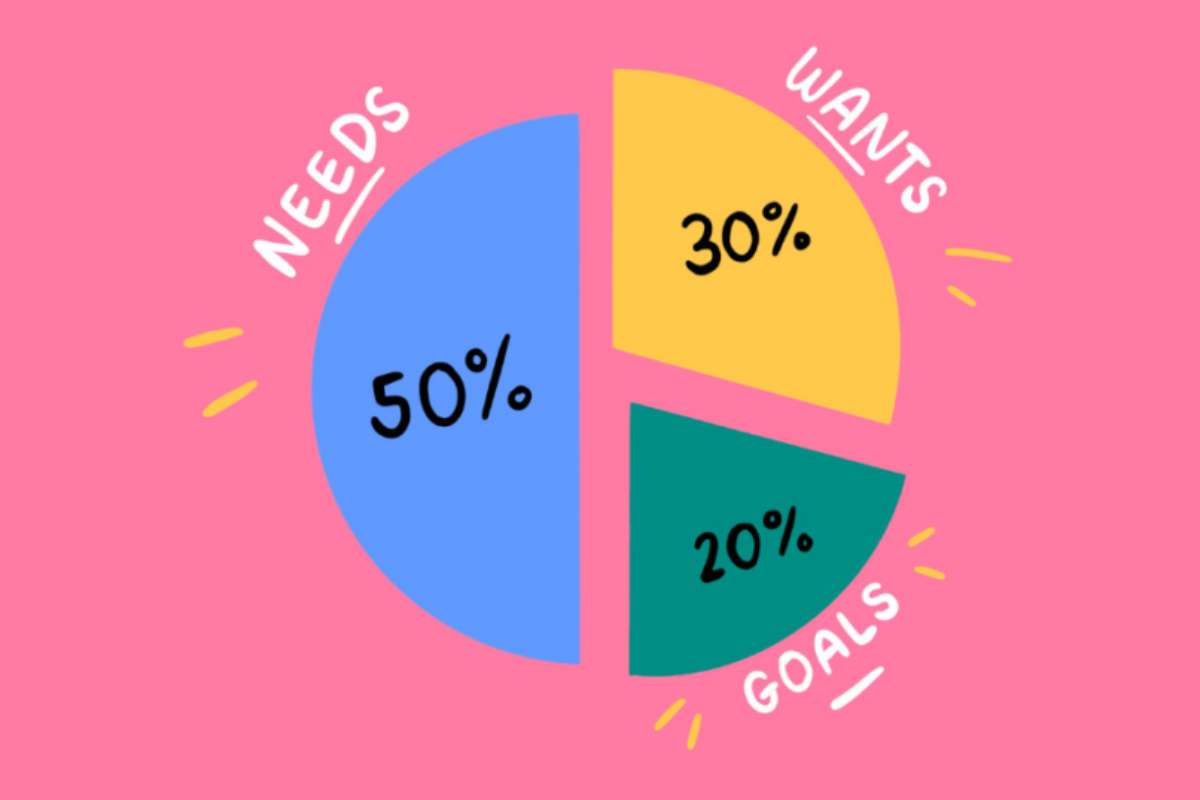

The 50/30/20 rule offers a straightforward approach to family finance management that many families find helpful. This method divides your after-tax, take-home income into three categories. Fifty percent goes to your needs, such as rent or mortgage, groceries, utilities, insurance, and transportation. Thirty percent covers your wants, such as dining out, entertainment, streaming services, and hobbies. The remaining twenty percent is allocated toward financial goals, including savings, debt repayment, and investments. If you have significant debt or high expenses, consider adjusting your budget to 80/10/10 until you’ve reduced your debt and built up your savings.

The most important part of family finance management isn’t which method you choose. It’s about picking one and sticking with it long enough to see results. Most people need about two to three months to adjust to a new budget. Don’t get discouraged if your first attempt isn’t perfect. Budgeting is a skill that improves with practice.

2. Creating a Budget Your Whole Family Can Support

One of the biggest mistakes people make with budgeting is treating it as a solo project. The best approach to family finance management involves everyone in your household. When your spouse, teens, and even younger children understand the family’s financial goals, they’re more likely to support them.

Start with a family meeting. Sit everyone down and explain why you’re creating a budget, without making it sound like punishment or deprivation. Frame it around your family’s values and goals. You can save for a vacation, pay off debt, or build an emergency fund. When each family member understands how their spending choices affect the whole family, they become invested in the plan.

During this meeting, discuss the difference between needs and wants. Help your children understand that needs are things you must have to survive and be healthy, like food, shelter, and clothing. Wants are things you’d like to have but can live without, such as a new video game or trendy clothing item. This distinction is crucial for family finance management because it trains your brain to think before making a purchase. Having this conversation early also prevents arguments later when you need to say no to purchases.

Assign roles and responsibilities. Your spouse handles bill payments while you manage grocery shopping. Perhaps an older teen tracks entertainment spending. When people have ownership of specific budget categories, they’re more engaged and accountable. This approach to family finance management also teaches everyone valuable skills they’ll need as adults.

3. Emergency Funds: Your Financial Safety Net

Life throws surprises at every family. Your car needs an unexpected repair, someone loses a job temporarily, or a medical bill arrives unexpectedly. Without an emergency fund, these situations become financial crises that derail your whole family’s financial management plan. That’s why building an emergency fund is non-negotiable.

Start by saving three to six months of essential living expenses. This includes your basic needs, such as housing, food, utilities, and transportation, but not wants, like vacations or hobbies. If your monthly essentials total $2,000, aim for a fund of $6,000 to $12,000. This might sound like a lot, but you don’t have to build it all at once. Start small with whatever amount you can afford each month, even if it’s just fifty dollars. Consistency matters more than the amount.

Keep your emergency fund in a separate savings account, ideally at a different bank than your checking account. This separation serves two purposes. First, it makes the money less tempting to spend on non-emergencies. Second, it’s easily accessible when you genuinely need it, but not so convenient that you raid it for groceries or a new purchase. Many families automate their emergency fund deposits, setting up an automatic transfer of money each payday. This removes the temptation to spend money you were planning to save.

4. Managing Debt and Protecting Your Family’s Finances

Debt can become a serious threat to your family’s financial management efforts if left unchecked. High-interest credit card debt can quickly spiral out of control. The average American family carries substantial credit card debt, and the annual interest charges can amount to thousands of dollars. When you’re working on family finance management, paying down high-interest debt should be a priority after you’ve covered your basic needs and started an emergency fund.

Look at each debt you carry and list them by interest rate, starting with the highest. Focus on paying the minimum on all debts, then allocate any extra money toward the debt with the highest interest rate. Once that’s paid off, move to the next one. This method, called the avalanche method, saves you the most money on interest over time. An alternative approach, called the snowball method, focuses on paying off the smallest balances first, which can be more motivating since you see victories more quickly. Choose the approach that feels most sustainable for your family.

5. Using Technology to Simplify Family Finance Management

Technology can be a powerful ally in family finance management, especially in 2025, when numerous user-friendly tools are available. Apps like YNAB, Goodbudget, and Monarch Money make it easy to track spending, set goals, and involve multiple family members in the process. These apps send notifications when you’re approaching your budget limits and give you real-time updates on your spending.

Don’t feel pressured to use the fanciest app. A simple spreadsheet works just fine if you prefer. The best tool for family finance management is the one you’ll actually use consistently. Whether it’s an app or a spreadsheet, what matters is that you’re tracking your money and staying aware of your spending patterns. In 2025, many new AI-powered budgeting tools can even predict your spending and offer personalized advice, but these are optional extras, not requirements.

6. Planning for Major Goals and the Future

.jpg)

Effective family finance management includes planning for the future. This might mean saving for your child’s college education, planning for retirement, or saving for a down payment on a home. These goals require both a timeline and a specific savings amount.

Work backward from your goal. If you want to save twenty thousand dollars for a home down payment in five years, you need to save about three hundred thirty-three dollars per month. Automate these savings by setting up a separate account and automatic transfers. Having money transferred automatically before it appears in your checking account makes saving much easier.

7. Keeping Your Family Finance Management Plan on Track

Creating a budget and a plan is one thing. Actually sticking to it is another. Most families find it helpful to review their budget on a monthly basis. Set a regular time, such as the first Sunday of each month, to review your spending and make adjustments as needed. During this review, celebrate the areas where you stayed on track and discuss challenges without blame. The goal is progress, not perfection.

Life changes, and your budget should too. When your income increases, don’t automatically increase your spending by the same amount. Instead, put at least a portion of the extra money toward your savings goals or debt repayment. This is how many families gradually improve their financial position. Remember that family finance management is a journey, not a destination. There will be months when you overspend and months when you do great. What matters is that you’re aware and making an effort.

Conclusion

Taking control of family management gives you more than just financial security. It gives you freedom, peace of mind, and the ability to make choices based on your values rather than reacting to circumstances. Start where you are, use what you have, and do what you can. Your family’s financial health will improve when you go through the process. The tools exist, the methods are proven, and the benefits are real. Begin today, involve your family, and watch as your financial confidence grows month after month.